Starting Point: Dr. Joe's First-Person Analysis

"Many people, when they leave permanent employment (Section 33), are immediately afraid of losing their healthcare coverage — so they rush to sign up for voluntary social security, Section 39, without properly calculating what it costs them."

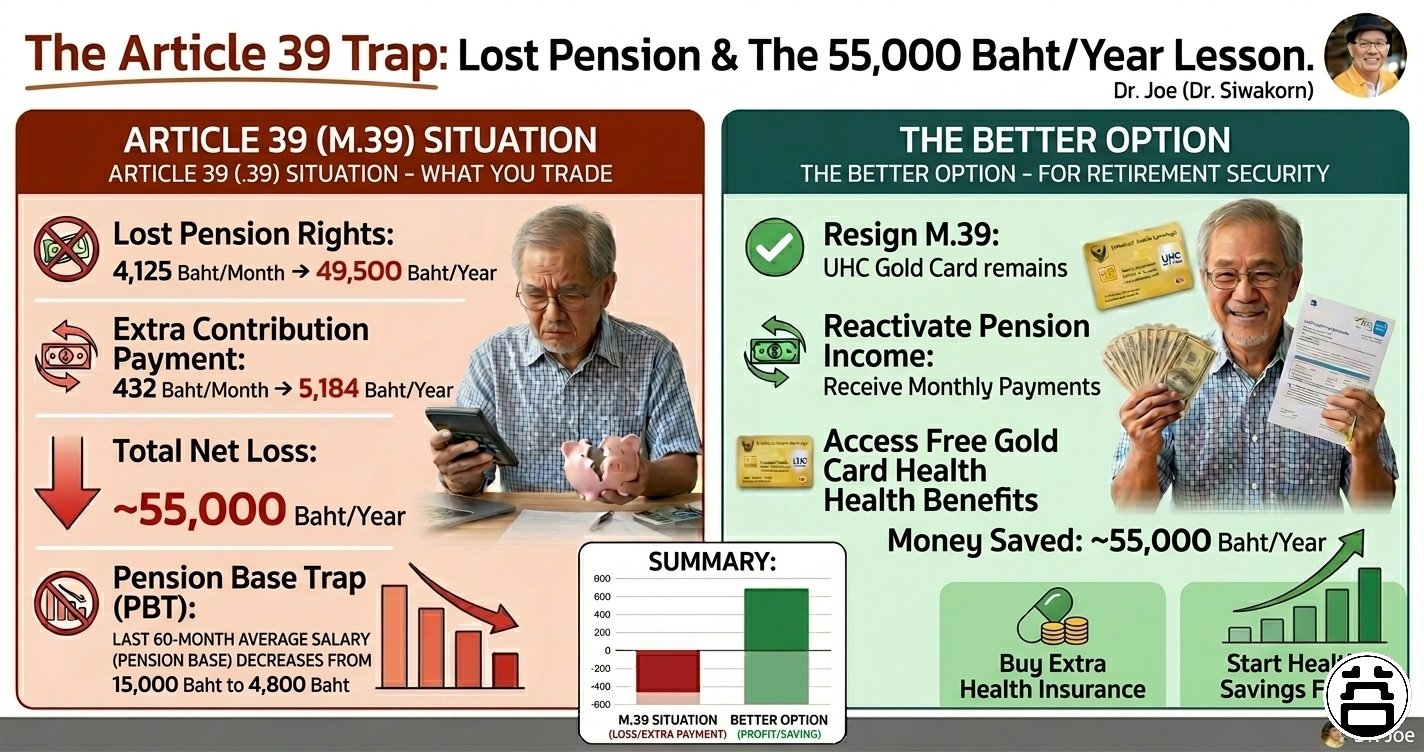

"When enrolled in M.39, I was classified as an 'insured person' — which meant I had no right to receive the old-age pension I had accumulated over my entire working life. My pension of 4,125 Baht/month was suspended + I was paying 432 Baht/month in M.39 contributions. Total loss: ~55,000 Baht/year."

"Your pension is the reward for a lifetime of hard work. Don't let it disappear simply because you don't understand the rules."

I agree completely with Dr. Siwakorn, and I want to extend his analysis by exposing the full three-layer mechanism of this trap — and providing a decision framework that covers every situation.

Layer 1: The Double Hit — Lose Pension + Pay More

This is the layer Dr. Joe discovered through personal experience. The numbers are direct and painful:

💸 The Double-Hit Equation: Paying Twice for One Benefit

Layer 1 — Pension Suspended:

4,125 Baht × 12 months = 49,500 Baht/year

Layer 2 — M.39 Contribution Paid:

432 Baht × 12 months = 5,184 Baht/year

──────────────────────────────────────────────

Total Cash Flow Lost:

49,500 + 5,184 = ~55,000 Baht/year

All of this to retain "Section 39 healthcare" — a benefit you already have access to for free through the Universal Health Coverage (Gold Card) scheme.

Layer 2: The Pension Base Trap — Permanent Damage

This is the more dangerous layer — one many people overlook because the pain isn't immediate. It is, however, permanent.

Thailand's social security pension is calculated from the "average salary of the last 60 months." While working under Section 33, your base may be 15,000 Baht (the current maximum). But Section 39 forces a fixed base of only 4,800 Baht.

🚨 The Pension Base Trap: Brutal Mathematics

Suppose you contributed under M.33 for 25 years (300 months) at a 15,000 Baht base,

then enrol in M.39 for 5 years (60 months) at the 4,800 Baht base.

The 60-month average is immediately dragged down:

→ Before: average 60 months = 15,000 Bt → Pension ~4,125 Bt/month

→ After 5 years of M.39: average 60 months ≈ 4,800 Bt → Pension ~1,300 Bt/month

Permanent monthly shortfall: ~2,800 Baht = ~33,600 Baht/year

Over 20 years of retirement (to age 75):

Total loss ~672,000 Baht

"Layer 2 doesn't just cost you money each year — it destroys the DNA of your pension permanently. Even if you leave Section 39 later, the damage to your 60-month average cannot be undone."

— Boon Arayapon, Dr. Boon

Layer 3: The Healthcare Misconception

The reason people rush into M.39 is fear of losing healthcare coverage. The reality: every Thai citizen automatically receives Universal Health Coverage (UHC / Gold Card) when they leave the social security system.

| Healthcare Benefit |

M.39 (Costs Money) |

Gold Card (Free) |

| Outpatient (OPD) | ✓ Covered | ✓ Covered |

| Inpatient (IPD) | ✓ Covered | ✓ Covered |

| Cancer / Serious Disease | ✓ Covered | ✓ Covered |

| Emergency / Accident | ✓ Covered | ✓ Covered |

| Dialysis / Kidney Failure | ✓ Covered | ✓ Covered |

| Local Public Hospital | ✓ Available | ✓ Available |

| Annual Cost | 5,184 Baht | Free |

| Pension Received | ❌ Suspended | ✓ Received immediately |

The marginal advantage of M.39 over Gold Card comes down to access to certain hospitals and minor dental coverage. With ~55,000 Baht/year saved, you can purchase private health insurance that covers far more than M.39 — with your choice of hospital.

Decision Framework: Should You Join Section 39?

Not everyone should leave M.39 immediately — it depends on your situation. Use this framework before deciding:

🧭 Decision Framework — Before Joining Section 39

Q1

Have you already contributed for 180 months (15 years)?

→ Not yet: Consider staying in M.39 to reach pension eligibility (but watch Layer 2)

→ Yes: Go to Q2

Q2

Are you still within the first 60 months after leaving M.33?

→ Past 60 months: Exit M.39 immediately — your pension base is being eroded

→ Within 60 months: Go to Q3

Q3

What is your monthly pension entitlement?

Calculate: pension × 12 months vs M.39 contribution cost (5,184 Baht/year)

→ Pension much higher: Leave M.39 and collect pension instead

→ No pension right yet: M.39 may be temporarily appropriate

Q4

Do you have a chronic condition requiring treatment at a specific hospital?

→ No: Gold Card is sufficient — no need for M.39

→ Yes: Compare against a private health insurance plan first

Three Smarter Strategies

✅ 3 Strategies That Beat Staying in M.39

1

Exit M.39 + Collect Pension Immediately

File at the Social Security Office — your pension will be paid from the following month. Your Gold Card healthcare rights are restored automatically. Instant cash flow gain: 4,125 Baht+/month with no additional steps required.

2

Use Gold Card + Private Health Insurance

Gold Card covers all serious illnesses. If you want added convenience, use the ~55,000 Baht/year you save to buy private OPD+IPD health insurance — you get hospital choice and far broader coverage than M.39 provides.

3

Invest the ~55,000 Baht/Year Difference

If you invest 55,000 Baht/year in RMF/SSF funds or high-yield deposits over 10 years (4% average return), you will accumulate over 660,000 Baht in additional savings — the tangible difference between understanding the rules and not understanding them.

Dr. Boon's Perspective: Connecting to the 3-Request Policy

🔍 Systemic Analysis: Why Does This Trap Still Exist?

⚙️

The System Doesn't Warn You

The Social Security Office has no automatic alert system to tell you "joining M.39 will suspend your pension." Workers must know on their own — or be told by someone else. This is a systemic failure that must be fixed.

📋

Supreme Court Ruling 3307/2567 Helps Partially

The ruling established that M.33 pension rights must be preserved for life — the 4,800 Baht M.39 base cannot retroactively reduce M.33 entitlements. This protects certain cases, but does not resolve the suspension of pension while enrolled in M.39.

⚖️

The 3-Request Policy Is the Long-Term Fix

"Request to Choose" would allow insured workers to receive their pension even while enrolled in M.39 — eliminating Layer 1 of the trap immediately. "Request Legal Reform" would mandate that the system provide transparent information before anyone signs an M.39 form.

"Dr. Siwakorn took his personal pain and turned it into a public lesson. That takes courage — and it is exactly what Thailand's social security community needs: real data from someone who lived it."

— Boon Arayapon

Conclusion: Calculate First, Decide After

Before signing an M.39 application, answer these three questions:

❓ 3 Questions to Answer Before Joining M.39

1️⃣

Am I already eligible for a pension?

Check your contribution history via the SSO Plus app. If you've paid in for 180+ months, you may be about to suspend your own pension rights.

2️⃣

Is my monthly pension more than the M.39 contribution?

If your pension is 3,000+ Baht/month but M.39 costs you 432 Baht/month, why accept the trade?

3️⃣

Is my free Gold Card truly not enough?

If you want more convenience, the ~55,000 Baht/year you save can buy private health insurance that's significantly better than M.39.

🧮 Calculate Your Gratuity & Pension Now

Use the calculator developed by Dr. Boon — see your actual figures before making any decision.

Covers M.33 / M.39 / M.40 with 28 years of real compound interest rates.

Frequently Asked Questions (FAQ)

Do I need to join Section 39 to keep healthcare after leaving my job?

Not necessarily. Every Thai citizen automatically receives Universal Health Coverage (UHC / Gold Card) when they leave the social security system, covering all serious illnesses. Before joining M.39, calculate the full financial impact first.

How dangerous is the Pension Base Trap in Section 39?

Extremely dangerous because the damage is permanent. If you stay in M.39 for more than 60 months, the 4,800 Baht base is blended into your 60-month average. A pension that should be 4,000–5,000 Baht/month can drop to 1,000+ Baht/month forever. Over a lifetime, the total loss can exceed 600,000 Baht.

What does Supreme Court ruling 3307/2567 mean for M.39 members?

The ruling protects M.33 pension rights for life — the 4,800 Baht M.39 base cannot retroactively reduce M.33 entitlements. However, it does not resolve the core issue: pension is still suspended while you are actively enrolled in M.39. That's why the 3-Request Policy is critical.

If I leave M.39, when does my pension start?

If eligible (180+ months contributions + age 55 + end of insured status), file with the Social Security Office. Your pension starts from the following month. Your Gold Card (UHC) rights are automatically restored — no separate application needed.

What if I haven't yet reached 180 months of contributions?

If you haven't reached 180 months, staying in M.39 to accumulate enough for pension eligibility may be worth it — but with caution: (1) Don't let M.39 exceed 60 months after leaving M.33 if you had a high M.33 salary base. (2) Calculate the break-even point. (3) Use the calculator at

calc-sso/ to run the numbers.

#Section39Trap

#PensionTrap

#55000Baht

#GoldCard

#PensionBaseTrap

#Ruling3307

#3RequestsPolicy

#BoonArayapon

#DrJoe

#ThailandSSO