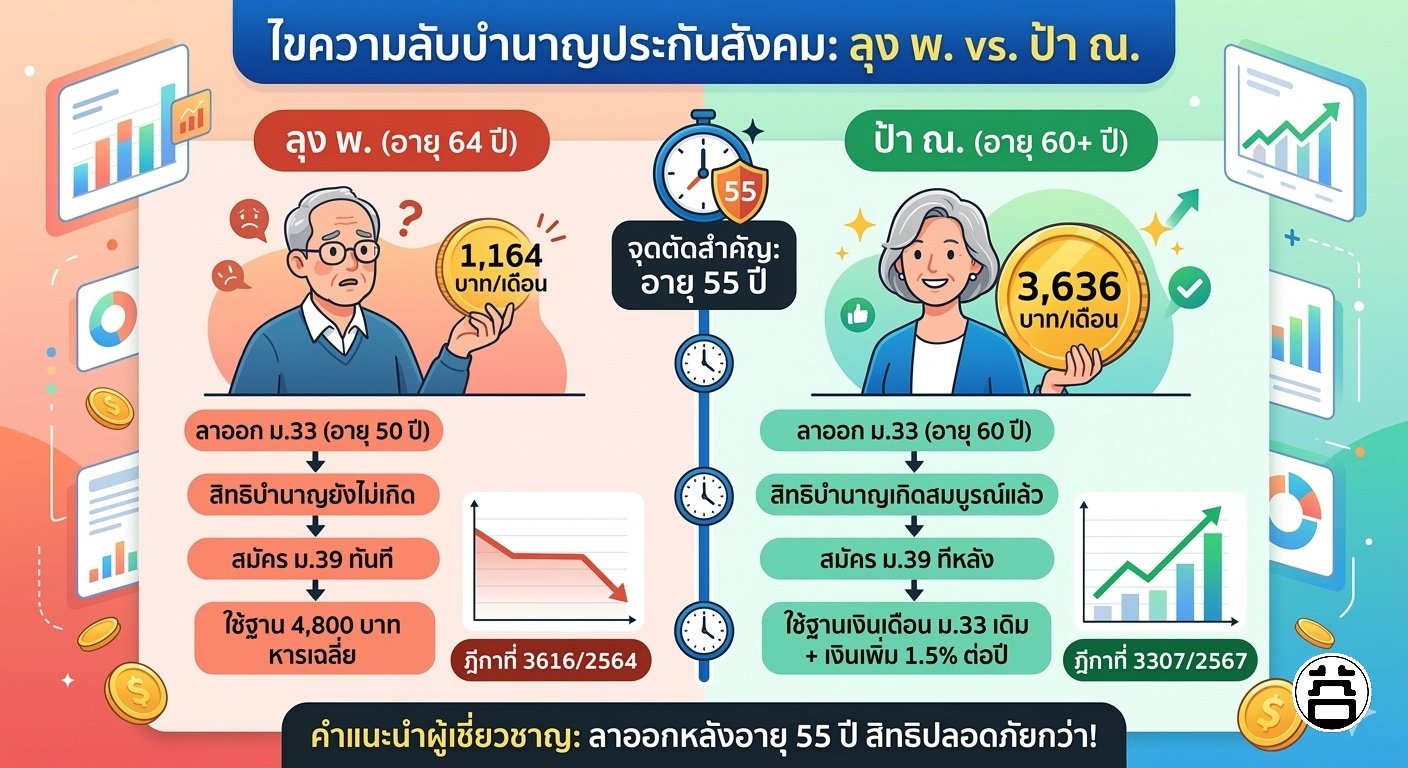

📖 The Puzzle: Same System, Drastically Different Pensions

Imagine two workers — both contributed to Thailand's Social Security for decades, both with similar salaries, both eventually enrolling in Section 39 (voluntary self-insured). Yet at retirement, one receives just 1,164 THB/month while the other gets 3,636 THB/month.

The answer lies in two landmark Supreme Court rulings. Understanding them could protect — or explain — your own retirement income.

1,164

THB/month

"Uncle P." received

Ruling 3616/2564

3,636

THB/month

"Aunt N." won

Ruling 3307/2567

Age 55

The critical threshold

Before = rights at risk

After = rights protected

🔴 Rights Lost

"Uncle P."

Ruling 3616/2564 · Mr. Pairoj P.

1,164

THB / month

Left Sec. 33 employment at ~age 50

Pension rights not yet vested at departure

Enrolled Sec. 39 immediately (base: 4,800 THB)

Supreme Court upheld SSO's averaged calculation

🟢 Rights Protected

"Aunt N."

Ruling 3307/2567 · Ms. N.

3,636

THB / month

Left Sec. 33 employment at age 60

Pension rights already fully vested

Enrolled Sec. 39 later — added 1.5%/yr bonus

Supreme Court: use original Sec. 33 base wage

😔 The Trap: "Uncle P." and the 4,800 THB Dilution Problem

Mr. Pairoj (our "Uncle P.") worked for ESS Electronics (Thailand) Co., Ltd., earning 15,000 THB/month. Around age 50, he resigned and enrolled in Section 39 (the voluntary continuation scheme) — a sensible move to keep health coverage.

⚖️ Ruling 3616/2564 — How the Calculation Worked Against Him

Sec. 33 wages

15,000 THB × 54 months in the final 60-month window

Sec. 39 base

4,800 THB × 6 months — pulled the average sharply down

Average wage = (15,000×54 + 4,800×6) ÷ 60 = 5,820 THB

Pension = 5,820 × 20% = 1,164 THB/month

📌 Supreme Court's ruling: Since Uncle P. was a Section 39 member during the final 60-month calculation window, the 4,800 THB deemed wage was legitimately included in the average. The court upheld the SSO's calculation.

🧮 Calculate Your Own Pension Estimate

Use Dr. Boon's SSO calculator — 28 years of real Royal Gazette interest rates, lump sum vs pension comparison, and Breakeven Age. Supports both Section 33 and Section 39 histories.

🔢 Open SSO Calculator

📊 Compare Gratuity vs Pension

🏆 The Victory: "Aunt N." and Why Timing Was Everything

Aunt N. worked at a hotel company with an average monthly wage of 13,222 THB. Unlike Uncle P., she stayed in her Section 33 job until age 60 — five full years past the critical threshold. She then enrolled in Section 39 on the advice of an SSO official.

"The pension rights of the plaintiff had already fully vested. Her subsequent enrollment in Section 39 can only serve to increase those rights — not diminish them."

— Principle from Supreme Court Ruling 3307/2567

The SSO initially tried to pay her just 1,320 THB/month — applying the same averaging logic as Uncle P.'s case. Aunt N. fought all the way to the Supreme Court and won 3,636 THB/month.

⚖️ Ruling 3307/2567 — The Correct Calculation

Base entitlement

13,222 THB avg wage × 20% = 2,644.40 THB/month (vested before Sec. 39 enrollment)

Section 39 bonus

60 months = 5 years × 1.5% = 7.5% → 13,222 × 7.5% = 991.65 THB/month added

Total pension = 2,644.40 + 991.65 = 3,636.05 THB/month

📌 Key principle: Once pension rights are fully vested (age 55+ with ≥180 months contributions), Section 39 enrollment afterward can only ADD to the rate at 1.5% per 12 months — the original Section 33 wage base must be preserved.

⚖️ Side-by-Side: The Age-55 Divide

| Factor |

🔴 Uncle P. (Rights Reduced) |

🟢 Aunt N. (Full Rights) |

| Left Sec. 33 |

Before 55 (~age 50) |

After 55 (age 60) |

| Rights at departure |

Not yet vested — age <55 |

Fully vested before exit |

| Section 39 impact |

4,800 THB averaged into 60-month window |

1.5%/yr bonus on original base only |

| Effective wage used |

5,820 THB (dragged down from 15,000) |

13,222 THB (original Sec. 33 wage preserved) |

| Monthly pension |

1,164 THB |

3,636 THB |

| Ruling reference |

3616/2564 |

3307/2567 |

💡 What This Means for You: Practical Guidance

If you're still employed, wait until at least age 55 before resigning. Leaving before 55 means your pension rights have not vested. If you then enroll in Section 39, the 4,800 THB base gets averaged into your pension calculation — potentially cutting it by 60-70%.

If you left Section 33 after age 55 (rights fully vested) and then enrolled in Section 39, but the SSO is averaging the 4,800 THB base — you have legal grounds to challenge this, citing Ruling 3307/2567.

While Ruling 3616/2564 upheld the SSO's position, Ruling 3307/2567 established a new principle: "vested rights cannot be reduced." If an SSO officer recommended Section 39 enrollment without explaining the pension impact, you may have grounds to argue official negligence in your complaint.

🔢 Know Your Numbers Before Filing Any Complaint

Calculate your actual entitlement first. The SSO calculator covers both lump sum (บำเหน็จ) and monthly pension (บำนาญ), shows your Breakeven Age, and uses 28 years of real interest rate data.

🧮 Open SSO Calculator

🔥 Why Ruling 3307/2567 Matters Beyond This One Case

🎯 Key Legal Principles Established by Ruling 3307/2567

Vested rights are immutable: Once a worker reaches age 55 with ≥180 months of contributions, the pension entitlement is legally fixed. It cannot be averaged down by subsequent Section 39 enrollment.

Section 39 = enhancement only: Voluntary continued enrollment after vesting can only add to the pension rate (at 1.5% per 12 months on the original base wage). It cannot trigger recalculation of the base.

Official guidance creates legal obligations: The court considered that Aunt N.'s delayed filing was reasonable because an SSO officer directed her to continue paying into Section 39. State negligence in guidance has legal consequences.

Different facts = different outcomes: The court explicitly noted that Ruling 3616/2564 applies to different factual circumstances. The two rulings coexist — each applies to its specific scenario.

⚖️ Quick Rule: When Does Section 39 Help vs Hurt?

Dangerous

Leave Sec. 33 before age 55 and immediately enroll in Sec. 39 — the 4,800 THB base gets averaged into your final 60-month window, potentially cutting your pension drastically.

Safe

Leave Sec. 33 after age 55 (rights fully vested) and then enroll in Sec. 39 — you receive a 1.5% annual bonus on your original base wage, with no averaging penalty.

Legal path

If you left Sec. 33 after age 55 but the SSO is averaging your pension incorrectly — cite Ruling 3307/2567 and file a formal complaint with your regional SSO office.

❓ Frequently Asked Questions

How do I check what age I was when I left Section 33?

You can verify via: (1) Your employment certificate or salary records, (2) Your SSO contribution history at www.sso.go.th, (3) Filing a formal records request with your regional SSO office using form สปส. 1-10/1.

I left Section 33 before age 55 — can I go back to work and re-enroll?

It depends on your current age. If you are under 60, you can return to employment as a regular employee and re-enroll in Section 33 — this resets your contribution window and can significantly improve your pension base. If you are already 60 or older, the law prohibits new enrollment in Section 33 as a first-time member. At that point you would need to explore other options, such as filing a complaint citing official negligence, requesting a formal recalculation, or consulting a labour law attorney about your specific situation.

I'm in Section 39 now — does Ruling 3307/2567 automatically apply to me?

It applies only if you left Section 33 after age 55 with ≥180 months of contributions, then enrolled in Section 39, and the SSO is averaging the 4,800 THB base into your 60-month window. If you left Section 33 before age 55, Ruling 3616/2564 is the applicable precedent and the averaging method is upheld by the Supreme Court.

What if an SSO officer told me to enroll in Section 39 and I lost pension rights?

This is one of the strongest arguments available to you. The Supreme Court in Ruling 3307/2567 found that official guidance which caused a worker to delay claiming or change enrollment was sufficient reason to accept a late filing. Document the advice you received — date, location, officer's name if possible — and include this in your written complaint to the SSO.

Where do I file a complaint if my pension was miscalculated?

(1) Submit a written recalculation request to your regional SSO office (สำนักงานประกันสังคมจังหวัด/เขต). (2) If rejected, appeal to the SSO Appeals Committee (คณะกรรมการอุทธรณ์) within 30 days. (3) If the appeal is denied, file with the Labour Court (ศาลแรงงาน) — cite Ruling 3307/2567 as your legal basis.

📣 The Bottom Line: Age 55 Can Change Everything

Aunt N.'s case is a landmark for Thailand's 24.9 million insured workers. The Supreme Court established clearly that social security benefits must not become a trap that reduces living standards in old age. If you or someone you know may have been miscalculated — share this article and take action.

💬 Follow Dr. Boon on LINE

⚖️ Section 39 Class Action